Topics

- Introduction

- What is GST Audit Form?

- Is it mandatory to file FORM GSTR 9C?

- Who should file and certify FORM GSTR 9C?

- Is interest and penalty payable on identification of additional tax liabilities during filing the audit form?

- Process of filing GSTR 9C

- Conclusion

Introduction

This is a great leap on the path of self assessment by the tax payers. It is yet to be seen how the audit in GST looks like. However we have brought for you a step by step guide on how to file the GST Audit Form(GSTR 9C). You might want to know who can file this form. Is it mandatory to file it? There may be other questions in your mind. You can expect to solve all your doubts related to this topic in this post. So let us start.

What is GST Audit Form?

GST audit by the professionals is basically a reconciliation of accounts of the taxpayer. All the figures declared by the taxpayer in returns GSTR 9, 9A, and 3B and audited Annual Accounts Statement is reconciled and certified by the professionals. This reconciliation has to be filed in FORM GSTR 9C. This form is an indicator for the tax authorities to find the correctness of the figures present in the returns of the registered person.

Is it mandatory to file FORM GSTR 9C?

All the taxpayers who have their annual turnover more than Rs. 2 crores have to mandatorily file GSTR 9C and submit their audited annual accounts to the tax department.

Who should file and certify FORM GSTR 9C?

FORM 9C is filed based on verified accounts and annual statement of the tax person. The details have to be filed and certified by a professional Chartered Accountant or a CMA.

Is interest and penalty payable on identification of additional tax liabilities during filing the audit form?

Only interest is applicable. Penalty is applicable when the same points are identified by the tax department. So it is better to conduct this audit in a transparent manner.

Process of filing GSTR 9C

GSTR 9C has two parts:

Part A is Reconciliation Statement

Part B is Certification by professionals

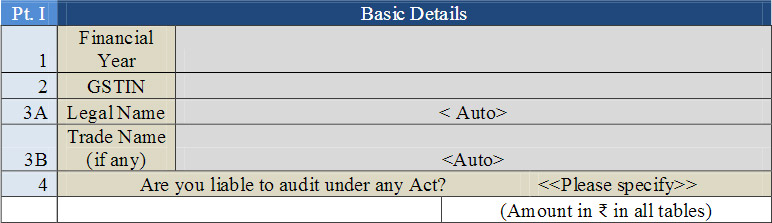

Part A: Reconciliation Statement looks as the screen shot given below. Part 1 of Part A of Reconciliation statement contains basic details like:

- Financial year – The year of which the details are provided in the form.

- GSTIN of the taxpayer- It is the GSTIN number of the taxpayer whose data is being analyzed.

- Legal Name of Registered person- The taxpayer must give his legal name. This is the name with which he has registered his company.

- Trade Name- There are entities who use one name for his trade but are registered in some other name. This is the name which the company uses while in trade.

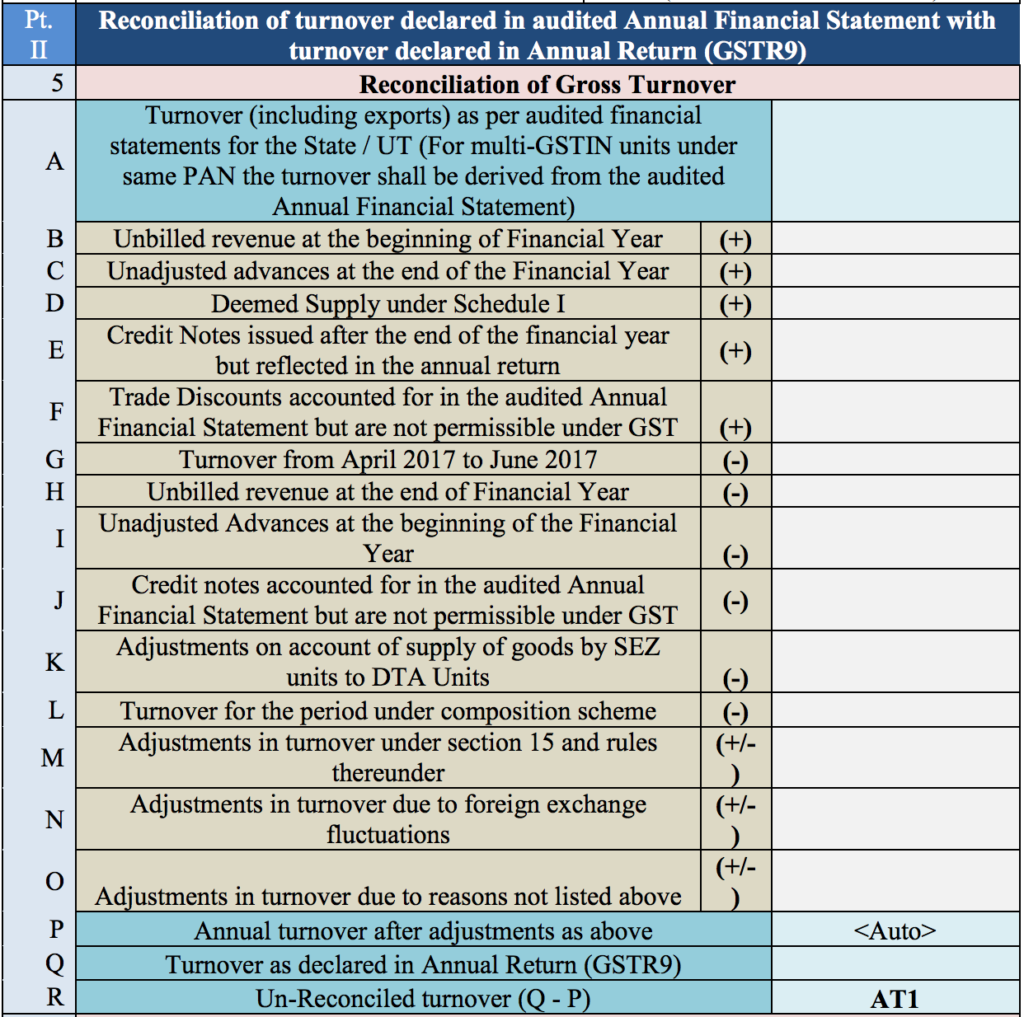

Part 2 of the reconciliation statement contains the actual reconciliation of the Annual Returns (FORM GSTR 9) with that of the Audited Annual Financial Statement of the taxpayer. Let us discuss all the fields mentioned in this part in a step by step way.

- 5.Reconciliation of Gross Turnover

- .5A.Turnover (including exports) as per audited financial statements. Here one this to note is the turnover is related to the State or Union Territory to which the GSTIN number of the taxpayer is mapped to. In usual case where an entity has presence over multiple states the Annual Financial Statement is consolidated for the entire business. In such cases the taxpayer is required to internally derive the turnover for that state or union territory and fill up the value. Not to mention that this value should also include the export turnover.

- .5B.Unbilled revenue at the beginning of the financial year –There are times where some revenue which were recorded earlier in the previous financial year are not part of the turnover of the Annual Financial Statement but GST is payable in the present financial (year under assessment). Such value needs to be declared in this field.

- .5C.Unadjusted advances at the end of the financial year –There are situations where the GST on advances are paid but they are not recognized as revenue in the Annual Financial Statement. Declare such values over here. For example for construction industry certain advances are received from the clients year on year as the development work progress. In Annual Financial Statement such revenue are treated as work in progress and does not figure in the turnover of the company until the entire construction is over.

- .5D.Deemed Supply under Schedule I – There are certain items which are present in schedule I which are considered as deemed supply. Goods and Service Tax are levied on such activities and value of such supplies is declared in this field.

- 5F.Credit Note issued after the end of the financial year-There is a possibility that credit notes are issued after the financial year is over but the supply has taken place in this financial year. Values of such credit notes are declared here.

- .5G.Turnover of April 2017 to June 2017 – If the Financial Year is 2017-18 then the turnover for the period April 2017 to June 2017 has to be declared so that while assessing the taxable amount such amounts which are beyond the GST period can be omitted.

- .5H.Unbilled revenue at the end of the financial year– Some unbilled revenue on which tax may be payable in the next financial year but is part of revenue in the current Annual Financial Statement has to be declared here. This value is deducted from the turnover while calculating the taxable value for the taxpayer

- .5I.Unadjusted advances at the beginning of the financial year- Value of all the advances where GST has not been paid in the current financial year but is recognized as revenue in the Annual Financial Statement.

- .5J.Credit Note accounted for the Audited Financial Statement but is not permissible under GST- This is the aggregate value of credit notes which is part of the Annual Financial Statement but is not admissible under Section 34 of CGST Act,2017.

- .5K.Adjustment on account of supply of goods by SEZ units to DTA units.- If you are an SEZ unit and have made supply to any DTA unit then such supplies are not taxable in GST. You are required to declare value of such supplies over here. While calculating taxable value this value is deducted.

- .5L.Turnover of the period under composition scheme– A taxpayer may partially pay tax under composition scheme and partially under normal tax structure. The turnover of the entity under composition scheme has to be deducted from the turnover to arrieve at the taxable value in FORM GSTR 9. So this value is declared in this field.

- .5M.Adjustment in turnover under section 15 and rules thereunder-This is the difference between the reported turnover in the Annual Financial Statement and the turnover reported in the Annual GST returns (GSTR 9 ) due to difference in the value of supply.

- .5N.Adjustment of turnover due to foreign exchange fluctuation: This is the difference between the reported turnover in the Annual Financial Statement and the turnover reported in the Annual GST returns (GSTR 9 ) due to foreign exchange fluctuation.

- .5O.Adjustment of turnover for reason not listed above: This is the difference between the reported turnover in the Annual Financial Statement and the turnover reported in the Annual GST returns (GSTR 9) due to any other reason which is not listed above.

- .5P.Annual turnover after adjustment as above- This is an auto populated field which is calculated from the values declared above. It is calculated as5P= 5A+5B+5C+5D+5E+5F-5G-5H-5I-5J-5K-5L(+/-)5M(+/-)5N(+/-)5O

- 5Q.Turnover as declared in Annual Returns (GSTR 9): Annual turnover as declared in GSTR 9 is declared here. It is calculated from the values declared in Sr. No. 5N, 10 and 11 in FORM GSTR 9.

- 5R.Un-reconciled turnover (Q-P): This field shows the difference between the value of 5P and 5Q. The reason for such difference is to be stated in the next section.

-

- 6.Reason for un-reconciled difference- The reason of un-reconciled amount as indicated in 5R is to be presented over here.

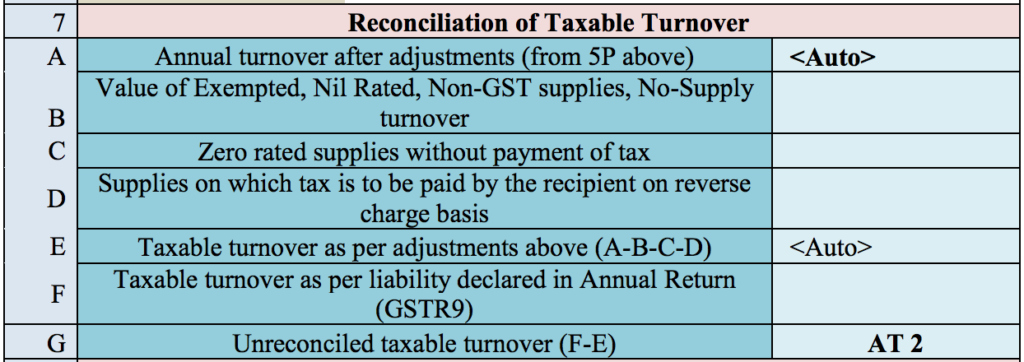

- 7.Reconcillation of Taxable turnover- Till this stage we have data to arrive at the total taxable output of the taxpayer. Now further data are required for arriving at the taxable turnover of the taxpayer.

- 7A Annual Turnover after adjustment – This field is auto populated from the figure generated in field 5P.

- 7B.Value of exempted, NIL rated, Non GST supplies, No supply turnover-Here the value of exempted, NIL rated, Non GST and no supplies has to be declared.

- 7C.Zero rated supplies without payment of tax-Here zero rated supplies are declared.

- 7D.Supplies on which tax has to be paid by the recipient on reverse charge basis- Here the value of inward supplies where tax is to be paid on reverse charge mechanism is declared.

- 7E.Taxable turnover as per adjustment above: This is calculated as 7E= 7A-7B-7C-7D. This field is auto generated.

- 7F. Taxable turnover as per liability declared in Annual Returns (GSTR9)- This is taxable turnover as declared in Table 4N of FORM GSTR 9.

- 7G. Un-reconciled turnover (7F-7E): This field shows the difference between the value of 7F and 7E. The reason for such difference is to be stated in the next section.

- 8.Reason for Un-reconciled taxable turnover- The reason for any difference in 7F and 7E has to be presented over here.

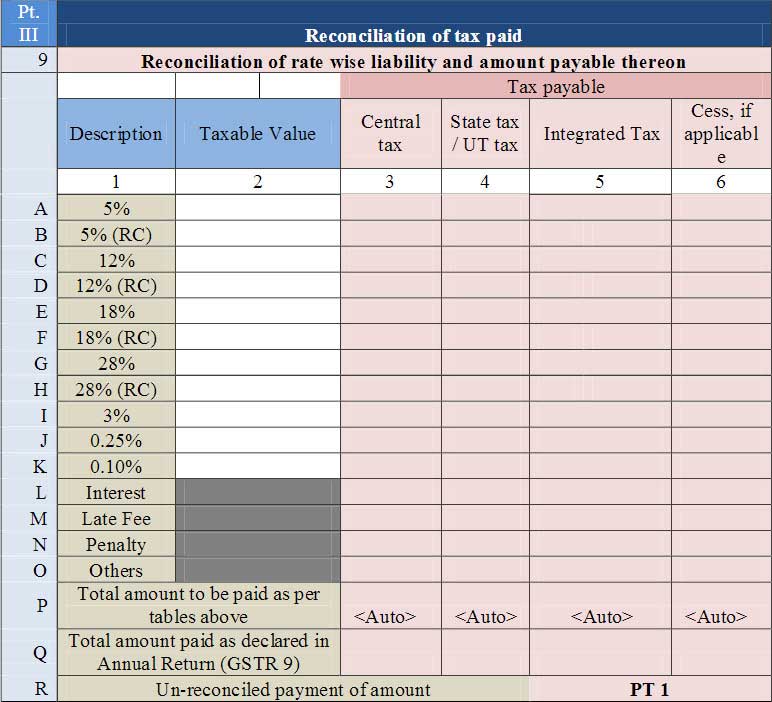

Part 3 is basically the reconciliation of tax paid by the taxpayer.

Part 3 is basically the reconciliation of tax paid by the taxpayer.- 9.Reconciliation of rate wise liability and amount paid thereon- It is basically the amount of tax paid by the taxpayer for different rate of Goods and Service Tax. The taxable value of each such supply has to be specified in this field. Further the taxable value and tax paid for inward supplies under reverse charge mechanism is to be specified over here. The tax payer also declares the value of any interest, penalty, late fee or any other tax payment made by the assessee in the financial year. Finally in field 9Q the value of tax paid by the tax payer as declared in FORM GSTR 9 has to be provided. Any un-reconciled amount of tax paid is calculated and auto populated in 9R. Reason for such un- reconciled amount has to be presented in the next section which is section 10.

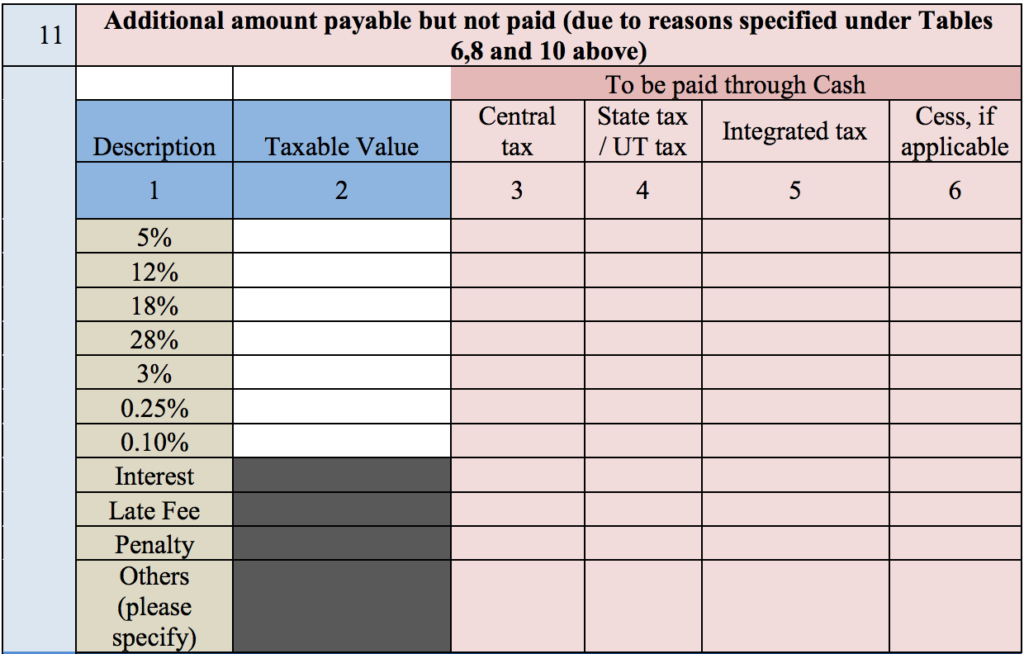

- 11.Additional amount payable but not paid (due to reasons specified under Table 6,8 and 10 above) – Here any additional amount payable but not paid due tp reasons presented in section 6,8 and 10 shall be declared here.

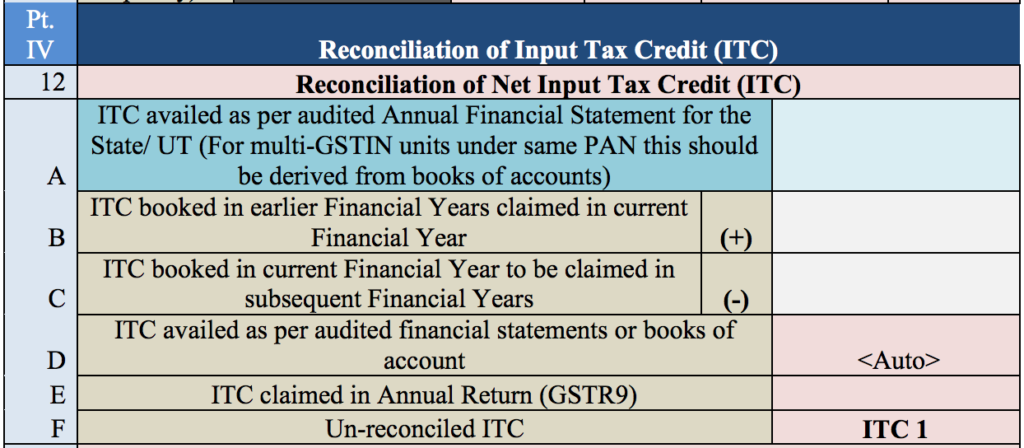

Part 4 is reconciliation of Input Tax Credit availed and utilized by the taxpayer under assessement

- 12A.ITC availed as per audited Annual Financial Statement for State/ UT – For a multi-location unit the Audited Annual Financial Statement contains reference of the Input Tax Credit (ITC) availed in respect to all the units related to that PAN. However in cases where such references are not present ITC availed has to be internally derived for each GSTIN and declared over here. The Input Tax Credit declared in this field is the total credit availed after reversals.

- 12B.ITC booked in the earlier financial year claimed in current financial year- This field should contain the Input Tax Credit declared in the earlier financial year but availed in this financial year.

- 12C.ITC booked in current financial year to be claimed in subsequent financial years-There may be ITC that has been declared in this financial year but is availed in the next financial year. Such Input Tax Credit is declared over here.

- 12D.ITC availed in audited financial statements or books of account- This is the auto populated field and is calculated as 12D=12A+12B-12C.

- 12F.ITC claimed in Annual Returns (GSTR 9)- This is the net ITC available as declared in Table 7J of GSTR 9(Annual Returns).

- 12G.Un-reconciled ITC – Any un-reconciled amount that is the difference between 12D and 12E figures out in this field.

- 13.Reason for any reconciled difference – In case of any un-reconciled amount as indicated in 12F, reasons for such a difference has to be presented over here.

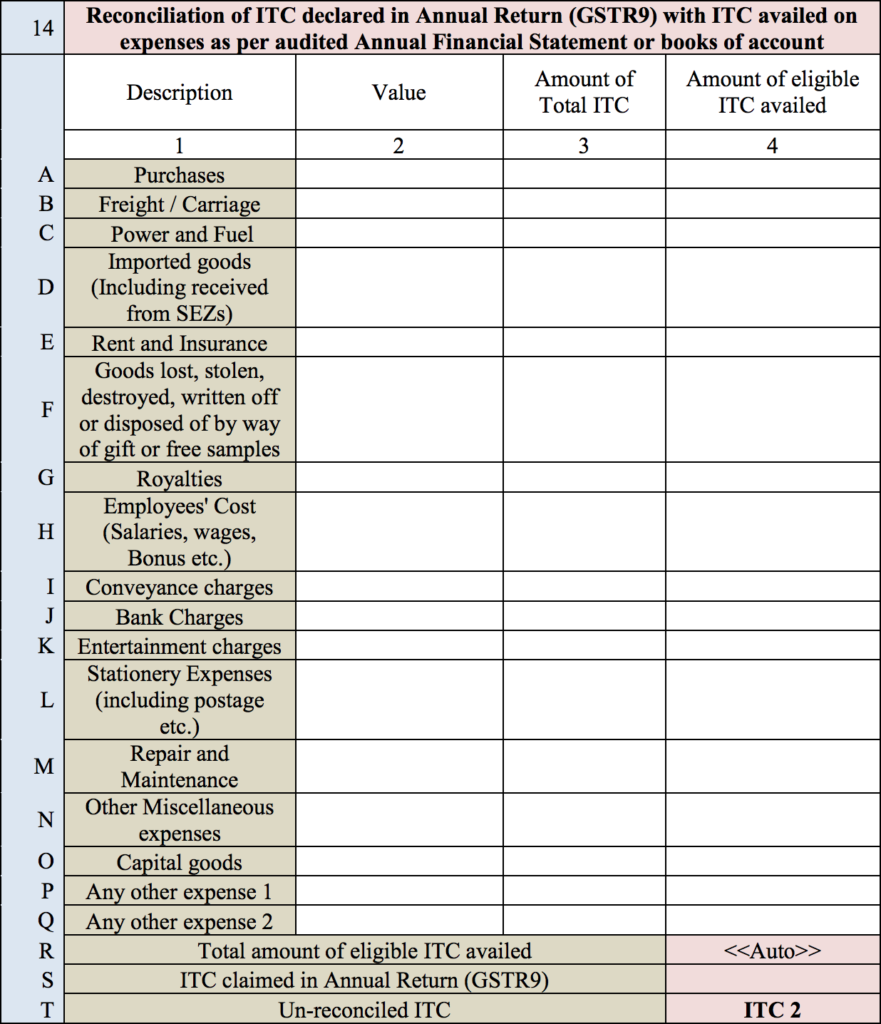

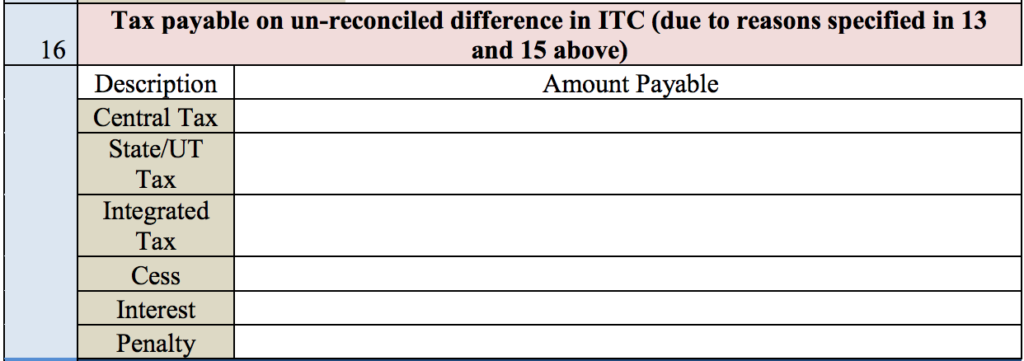

- 14I.Reconciliation of ITC declared in Annual Returns (GSTR 9) with ITC availed on expenses as per Audited Annual Financial Statement or books of accounts – This filed is basically the breakup of the Input Tax Credit availed for each input/ input services. For example you have to declare ITC availed on purchase, transport, rent etc. After all the values are fed into the table at last the total ITC availed is auto calculated. Finally any difference in the value declared in Annual Returns (GSTR 9) is indicated. Reasons for any such difference have to be provided in Table 15. Finally the value on which tax is payable due to reasons specified in table 13 and 15 is declared in table 16

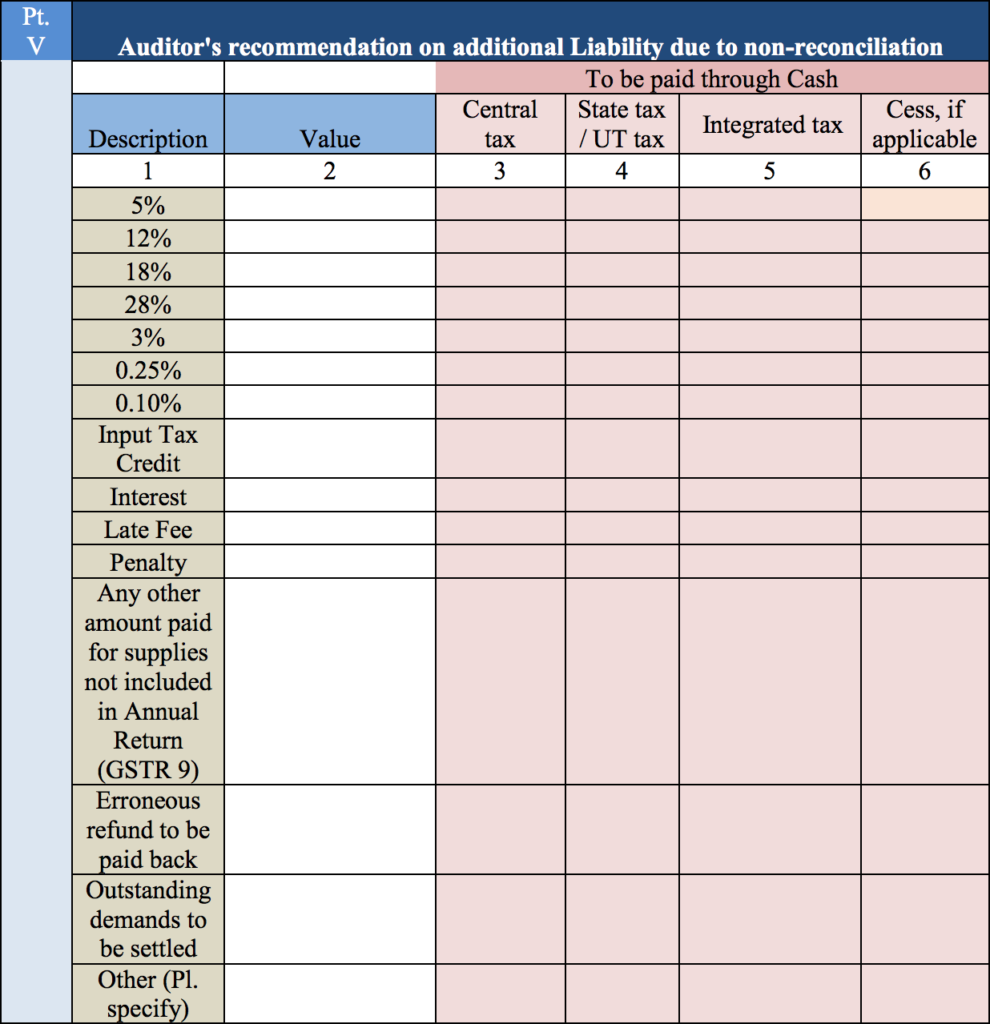

Part 5: Auditor’s recommendation on additional Liability due to non-reconciliation – Here the auditor’s recommendation on the tax payable due to un-reconciled turnover and un-reconciled Input Tax Credit is indicated. Any erroneous refund taken by the tax payer or any outstanding demand to be settled has to be declared over here. Finally the declaration has to be signed by the auditor who has verified and filled in the details.

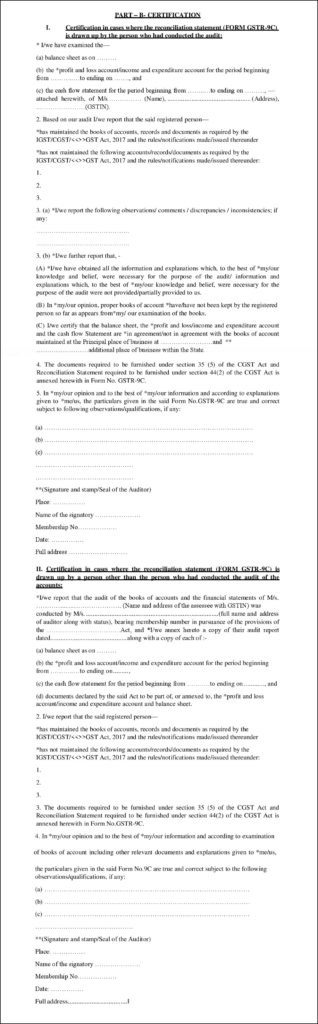

Part B: Certification

- 6.Reason for un-reconciled difference- The reason of un-reconciled amount as indicated in 5R is to be presented over here.

- The auditor who has verified the accounts certifies in this part regarding the documents maintained by the taxpayer is per the law. Further he declares the documents not maintained by the registered taxpayer. Further he should present his observations on the accounts and reconciliation presented above.

Conclusion

This is really a tiring piece to read and more tiring to perform. But I believe that the guidelines presented in the post would be a great help for tax person who are having a tough time figuring out what to do with GSTR 9C audit. Anyway you need to hire a CA or a CWA to take care of this form but an understanding of the form definitely helps to figure out the requirement. If you have any queries feel free to post.

-